The global automotive parts market has a low concentration ratio, with CATL leading with a 6% market share. China’s market size reached 5 trillion yuan in 2024, driven by growth in new energy and hydrogen energy, while intelligent suspensions are growing at an annual rate of 47%. Fuel systems still dominate, but policy and cost pressures are accelerating industry restructuring.

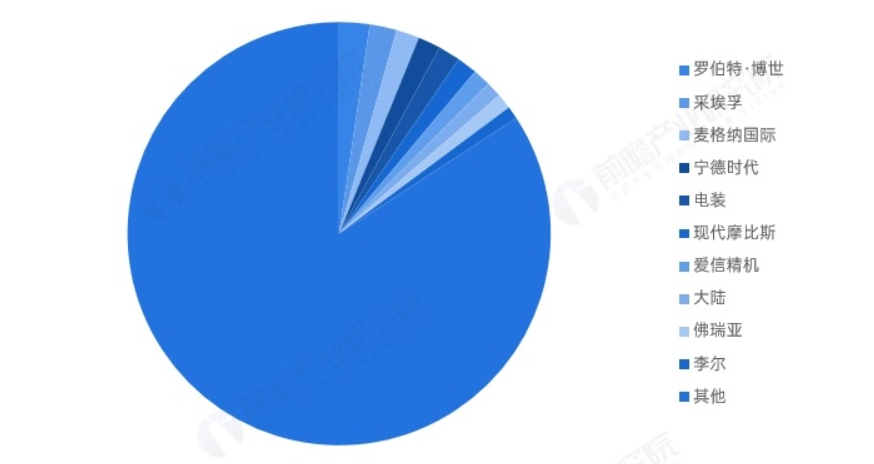

According to the 2024 global ranking data of automotive component suppliers, the top five enterprises are Bosch, ZF Friedrichshafen, Magna International, CATL, and Denso. In terms of the regional distribution of the top ten automotive component manufacturers, they are mainly concentrated in Germany, Japan and other regions, with their core businesses covering multiple fields such as automobile engines, autonomous driving, and automobile tires.

Top 10 Suppliers in the Automotive Parts Industry in 2025

| ranking | company | headquarters | Main layout |

| 1 | Robert Bosch | Germany | Mobile automotive solutions |

| 2 | ZF | Germany | Autonomous driving, body control |

| 3 | Magna International Inc. | Canada | Autonomous driving, Internet of Vehicles |

| 4 | CATL | China | Power batteries, energy storage batteries, battery materials and recycling |

| 5 | Denso | Japan | Vehicle driving data recorder, VSS, ECU |

| 6 | Hyundai Mobis | South Korea | The fields of autonomous driving, the Internet of Vehicles and electrification |

| 7 | Aisin Seiki | Japan | Autonomous driving, electronic powertrain |

| 8 | mainland | Germany | Intelligent Cockpit |

| 9 | Freya | France | Interior, seats, automotive electronics |

| 10 | Lear | United States | Seat system and components |

Based on data from major enterprises and market size, the market share of leading companies in the global automotive parts industry is generally below 3%. The market has a large number of enterprises with diverse business types, fierce competition, and overall low market concentration.

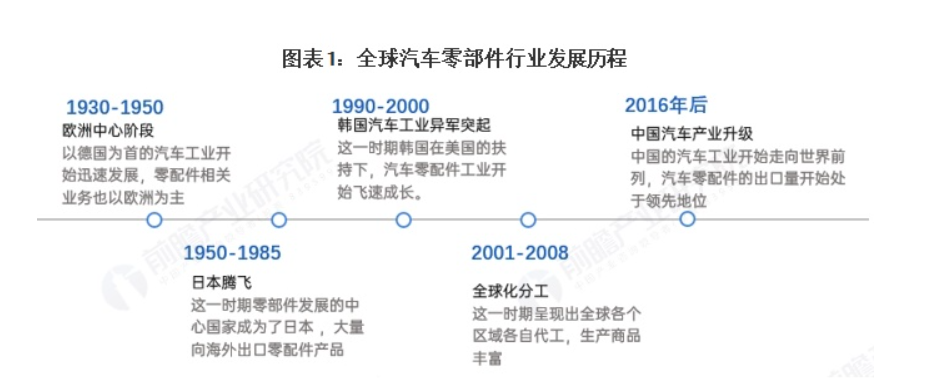

——Development History of the Global Auto Parts Industry:

The global automotive industry originated in Europe and the United States. The growth of the world automotive industry has undergone a long period of germination and development. Although automobiles were invented in Europe, the formation of the automotive industry marked by mass production took place in the United States, and later expanded to Europe, Japan and eventually the whole world. At present, China has become a major production region in the auto parts industry.

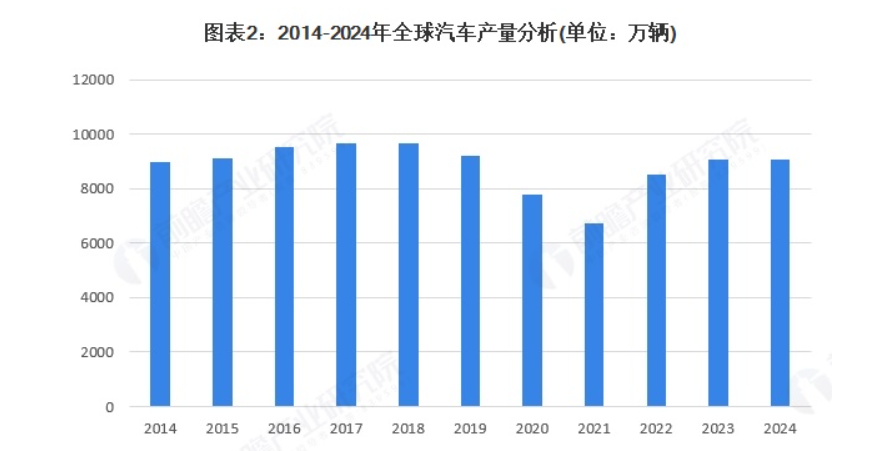

——Analysis of Global Automobile Production: Annual Output Exceeds 90 Million UnitsAt present

the global auto parts industry still exhibits a dominant enterprise effect. Large-scale enterprises such as Bosch, Denso, and Continental control the majority of global auto parts trade volume. The supply capacity of auto parts manufacturers exerts a decisive impact on downstream automobile production. From 2014 to 2023, global automobile production showed an overall upward trend, reaching 90.9 million units in 2023. Preliminary statistics indicate that global automobile production declined slightly in 2024, totaling 90.7 million units.

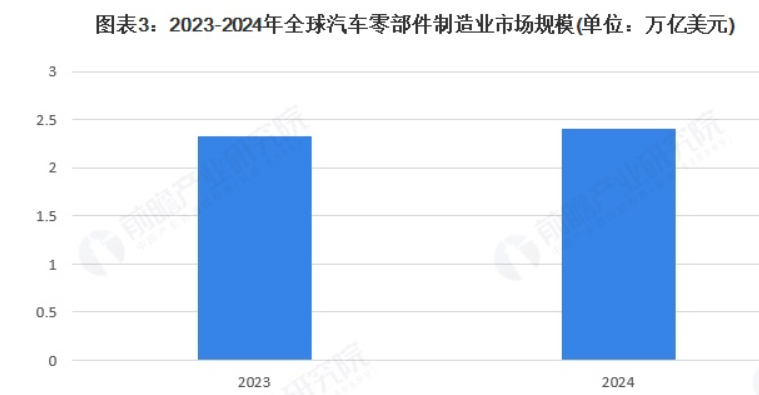

——Global Automotive Parts Market Size: Surpassing $2 TrillionWith increasingly fierce global competition

the automotive industries in developed countries around the world have undergone new changes, and the auto parts industry has also exhibited new characteristics such as group-based organization, high-tech advancement, systematic supply, and globalized operations. According to data from Business Research Insights, the global automotive parts market size stood at $2.33 trillion in 2023 and reached $2.41 trillion in 2024, representing a year-on-year increase of 3.43%.

Based on data from major enterprises and market size, the market share of leading companies in the global automotive parts industry is generally below 3%. The market features a large number of enterprises with diverse business types, intense competition, and low overall market concentration.